Frequently Asked Questions

You’ve got questions, we’ve got answers

About Alex Bank

So, what’s Alex Bank all about?

Alex Bank is here to build the future of banking, saying goodbye to complicated and slow processes - and hello to faster, fairer and more flexible banking options for Australians.

How is Alex Bank different from other banks?

Great question! We’re a bank built by an energetic team who have decades of experience inside traditional banks - meaning we’ve had a front row seat to what works, what doesn’t, and what’s possible. So, we know we’ve got what it takes to build Australians a better banking experience, that’s simple, easy to use and understand.

We’re a digital bank built from the ground up and not tied down by the ‘old banking ways'. Instead, we’ve built new ways, that make us more efficient, and that give you a better experience that saves you time, stress and those pesky banking fees!

We’re also not about to ‘set and forget it’ - we’re continually innovating new ideas to make your experience better. If you have a cool idea you’d like to share with us, email it to hello@alex.com.au

Who owns Alex Bank?

Founded by Simon Beitz CEO and Craig Fenwick, CFO in 2018 - we’re proudly independent and supported by a diversity of investors.

Is Alex Bank digital only, or do you have branches as well?

We’re 100% digital, and don’t have physical branches. So it’s easy to bank with us from your laptop or mobile at anytime, and from anywhere. It also means we don’t carry large overheads - so we can offer you better value products with no upfront or ongoing fees. But just because we’re digital-first, it doesn’t mean you can’t get a human helping hand if you need it.

To chat with our Australian-based customer service team, email us at hello@alex.bank or phone us on 13 ALEX.

Where is Alex Bank based?

Alex Bank is 100% Australian with offices in both Brisbane and Sydney.

Personal Loans

How is my personalised rate determined?

Rates are personalised depending on your credit history, financial circumstances and how much you are looking to borrow over what time. Take a look at our easy to use Loan Calculator to estimate your rate.

Does Alex Bank accept joint Personal Loan applications?

No, at this stage we only accept applications in individual names.

Can I apply if I don’t have suitable ID?

No, we must be able to identify you with an Australian Driver’s Licence or Australian Passport for our online ID systems to identify you securely.

Are there any fees?

We’ve made our personal loan as fair as possible with no ongoing or early repayment fees.

Check out all the fees we won't hit you with.$0 monthly account fees

$0 early repayment fees

$0 late payment fees

See our credit fee guide for more information.

How often can I pay off my loan?

We’re flexible. You can make weekly, fortnightly or monthly payments. You can also pay out your entire loan amount at any time without any extra fees. We won’t penalise you for getting ahead!

How much can I borrow?

You can borrow between $2,100 and $30,000 over a loan term between 6 months and 5 years. Find out what your repayments could look like here.

What are the eligibility requirements for an Alex Bank Personal Loan?

To be eligible applicants must be over 18 years old, be receiving a regular income, be an Australian Citizen or permanent resident and have not previously declared bankruptcy. Loan applications are subject to credit approval.

What do I need to apply for a personal loan?

If you are eligible to apply, you will need to ensure that you have the following :

A copy of your Australian Driver’s Licence or passport

The account number and BSB of where you’d like us to send your funds if approved

You’ll need a working camera on the device you are completing your application on so that we can verify your ID. i.e. laptop, mobile, tablet.

How long does it take for a personal loan application to be approved?

Usually within one business day, once we’ve received your full application and all documents.

How long after approval will the funds be in my account?

Once we receive your signed loan agreement the funds will be transferred. There is a standard processing time to transfer between banks, so while it’s immediate on our end it may take 1-2 business days to become available in your account.

How can I make payments into my account?

You can make payments via direct debit or direct transfer.

Can I apply for more than one personal loan at a time?

You can. We’ll work with you to understand your specific situation to determine if this is what you require or if there is another way to achieve what you are after.

What can I do if I'm having trouble passing the ID check?

Make sure you are entering your name, address and date of birth exactly as it appears on your ID. If you recently moved, make sure you have updated your address with the Australian Electoral Commission. If these tips don’t work, contact us at hello@alex.bank and we’ll try to help you.

What is a comparison rate?

A comparison rate includes the interest rate as well as certain fees and charges relating to a loan. The aim of the comparison rate is to help you identify the true cost of a loan and compare loans and services offered by financial institutions and mortgage providers.

Can I apply for a personal loan if I've been previously rejected?

You can, but depending on the timeframe and reason for decline the outcome may not change. You can speak to one of our team on 13 ALEX if you have specific questions in relation to your situation.

What is a credit score and why is it important to my application?

A credit rating or 'credit score' is a numerical score that represents how trustworthy your reputation is as a borrower. If you find out your credit rating through a credit agency, you will receive a number between 0 – 1,200 that summarises the information on your credit report at that point in time. A higher score means you have a good credit rating, with a lower score meaning you have an average to poor credit rating.

How do I check my credit score?

In Australia, there are three main credit reporting agencies: Equifax, Experian and illion, with different credit score ranges. Alex Bank uses Equifax to assess your credit worthiness. You can get more info here.

Should I check my credit score before applying?

It can be handy to understand your credit score and financial worthiness in general. Alex Bank only accept applications with higher than average credit scores. Your credit score is also one of many factors that we use to personalised your interest rate.

Do credit scores vary from different credit agencies?

Yes they do. Alex Bank uses credit ratings provided by Equifax.

How do I access my personal loan?

Log in to Alex Online or the Alex App. Contact us on 13 ALEX if you have not yet registered for Alex online banking.

Can I give permission for other people to access my account?

No, due to privacy regulations we can only speak with the related parties to an account and as we only have single borrowers available at this point in time, multiple internet banking logins aren’t possible.

I’m not comfortable connecting my bank statements digitally to finalise my application; can I provide you PDF statements instead?

Our bank statements feature allows us to verify your banking transactions within seconds. This feature is powered by illion who provide this solution to over 200 financial services providers in Australia and New Zealand. They use bank-grade security and no login information is seen or stored by Alex Bank.

Can I redraw from my Alex Bank personal loan?

No, unfortunately, any surplus funds in your Alex Bank personal loan account cannot be redrawn.

About our personal loan rates

What are some factors that Alex Bank use to calculate my overall rate?

Your Equifax credit score plus a range of information such as your transactional behaviour and employment stability.

Can I negotiate my rate with the Alex Bank team if I don’t like my initial offer?

We are always happy to speak with you regarding your offer. You can contact us at hello@alex.bank or on 13 ALEX.

I used the Alex Bank Personal Loan Calculator to get an estimate of my rate before applying, but my offered rate came back much higher than initially estimated. How can I understand the rate I’ve been offered?

There are many factors that could have influenced this. We are always happy to discuss your individual application result. Contact us at hello@alex.bank or on 13 ALEX to discuss.

Where can I find my credit score?

You can get your credit score for free from Equifax here.

Who can I talk to if I have questions about my credit score?

You can start with us at hello@alex.bank or on 13 ALEX, or contact Equifax directly.

Savings

How do I open an Alex Bank savings account?

Our Savings Account is open by invitation only. Please keep an eye out in 2024 for the official launch of our Savings product.

How do I add my Tax File Number (TFN) or check that it is recorded with Alex Bank?

The easiest way to add your TFN is during the application process. But if you forgot, don’t worry as you can also add it later through Alex Online.

To add your TFN or to check if it has been recorded, login to Alex Online and go to Settings. If a TFN is recorded it will be masked with *********.

If no TFN has been recorded it will show as ‘not provided’. Simply edit this section to add your TFN. Note that you will need to logout of Alex Online for the update to take effect.

Please logout, then log back in and return to the settings screen to check that your TFN is showing as *********.

Can I setup a Direct Debit from my Savings Account?

No, you cannot schedule a direct debit from your Savings Account.

How is interest calculated?

If interest is payable on your Account, it is calculated on a daily basis using the following formula:

Daily Closing Balance × (Interest Rate applicable to your Account ÷ 365)

The Daily Closing Balance is the credit balance of your Account at the end of a day. Interest is credited to your Account monthly at the end of a calendar month and on the day that the Account is closed.How do I setup my PIN?

You can set a PIN using the Alex App. Go to "Settings", under "Login" select "Change PIN", enter and verify your new PIN and then save.

How do I setup biometrics?

You'll first need to setup a PIN before you can setup biometrics (if supported by your phone). Go to Settings, under login select Change PIN, enter and verify your new PIN. Log out. Log in with your PIN then go to Settings, under Login enable biometrics. Ensure your phone is setup to accept this form of identification.

Do you have a Mobile Banking app?

Yes, our beta version Mobile Banking app is avaiable on both the App Store and Google Play Store.

How long does it take for my funds to be received in my Savings Account?

Although most funds are received on the same business day it can take up to three days to arrive depending on the issuing bank.

How long does it take for funds to leave my Savings Account?

All funds transfers are completed on the same business day so long as the transfer is initiated before 6pm AEST. Funds transferred on weekends or public holidays will not be actioned until the next business day.

Are there any deposit conditions on my Savings Account?

We don't have any deposit conditions on our Savings account to earn interest. For example, you don’t need to make a minimum monthly deposit and the rate does not expire after a honeymoon period.

Are there any fees on my Savings Account?

No. We don’t charge any fees on our Savings Account.

What is the limit for a savings account?

We currently have a limit of $250,000 for our Savings Account, in line with the Australian Government Guarantee. If you would like to deposit more than $250,000 into your account please contact us at hello@alex.bank

Is my account protected by the Government Guarantee?

The Australian Government guarantees aggregated deposits with Australian authorised deposit-taking institutions, which includes Alex Bank, for up to $A250,000 per person.

The Financial Claims Scheme (FCS) is an Australian Government scheme that was established during the 2008 global financial crisis to provide financial protection for consumers in the unlikely event of a failure of a bank, credit union, building society or general insurer.

The FCS provides protection for depositors of banks, credit unions and building societies that are incorporated in Australia (also known as authorised deposit-taking institutions or ADIs), for deposits up to $250,000 per account holder per ADI. The scheme aims to return deposits to account holders within seven days of activation of the FCS.

The FCS can be activated by the Australian Government in the unlikely event that an ADI or general insurer fails.

Once activated, the FCS will be administered by APRA.

The objectives of the FCS are to:protect depositors of ADIs, and claimants of general insurers, from potential loss in the unlikely event of the failure of these institutions;

provide depositors with prompt access to their deposits that are protected under the FCS; and support the stability of the Australian financial system.

Further information about the Government Guarantee can be obtained from the APRA website at www.fcs.gov.au.What is the daily transaction limit?

There is currently a $5,000 daily withdrawal limit to try and minimise any risk of fraud to our customers. If you would like to withdraw more than $5,000 at any time, please contact us at hello@alex.bank and our staff will assist you in performing the transaction at no additional cost to you.

Do you offer a physical card?

No, we do not offer a Physical Card on the Savings Account.

What are your contact hours?

Our contact centre is operational on business days between 9am - 5pm AEST Monday to Friday.

If you need to contact us outside of hours, you can contact us via our Online Chat or via our email and we will respond as soon as we are back online the next business day.

Who do I talk to about an issue with a payment?

Please email us at hello@alex.bank with the details or call our contact centre on business days between 9am - 5pm AEST Monday to Friday.

Term Deposits

Can I access my Term Deposit before the maturity date?

Term Deposits are designed to offer the certainty of a fixed rate for the agreed investment term.

They are not ‘at call’ which means you do not have access to your Term Deposit once it has been invested. Your funds are locked away for the agreed investment term.

Before opening a Term Deposit, if you reasonably expect that you will need access to your funds, a term deposit is not suitable for you.

However, should your financial situation change during the fixed term, you may request an early withdrawal of your funds prior to the maturity date provided that you give us 31 days’ notice. The notice period will start on the day you request the early withdrawal. We do not charge any fees for an early withdrawal but an interest adjustment will apply.

How do I open an Alex Bank Term Deposit?

Our Term Deposit product is currently only available for distribution via invite or selected Alex Bank-approved deposit Intermediaries. This means you will need to receive a direct invitation from Alex Bank or be a client of one of our Intermediaries to apply.

General Banking

What are Alex Bank’s opening hours?

Alex Bank’s regular office hours are Monday to Friday 8.30-5.00pm AEST, and closed on QLD public holidays. Leave us an email at hello@alex.bank, or a voicemail on 13 ALEX and we'll respond when we return to the office.

Can I access my accounts from overseas?

Yes. Just log into Alex Online.

Where can I view my personal loan interest rate

You can view the interest rate on your original contract. If you can’t find your original contract, just email hello@alex.bank.

Do you have an Alex Bank App?

Yes. You can download it for both Apple and Android phones.

Do you have Apple Pay / Google Pay?

We don’t currently have products that connect with Apple Pay or Google Pay, but we are working to launch new products that will in the near future.

Do you support PayID or Osko Payments?

We don’t currently support Osko or PayID. You can transfer money from other banks using our 259-000 BSB. You’ll need this BSB and your account number to transfer funds into an Alex Bank account.

Do you have a credit card account?

Currently, we don’t offer a credit card. But, watch this space.

Do you work with budgeting apps?

If your budgeting app supports using a banking account, you can nominate your savings account by using our BSB 259-000 and your account number. Please remember to always exercise caution when sharing your banking details with anyone, including an app or service provider.

Do you offer products for business use?

At this stage we only offer consumer products for personal use.

How do I change my account details or address?

If you would like to change your account details or address, just email hello@alex.bank and we can arrange this for you.

Do I get bank statements?

Yes, we provide statements every six months. Statements are provided at the end of the financial year and the end of the calendar year.

How do I access my Alex Bank bank statements?

To get your bank statements, you'll need to log in to your Internet Banking account and select the "statements" option to download them. Remember, statements are only issued twice per year, at the end of the calendar year on December 31st and at the end of the financial year on June 30th.

If you haven't yet registered for Internet Banking, please check the email we sent you when you received your loan funds titled "One last step. Set up your Internet Banking" for instructions. If you need any assistance with this process, please contact our customer support team at hello@alex.bank.

What is Alex Bank’s BSB number?

Our BSB number is 259-000

Security

How does Alex Bank protect my information?

Alex Bank uses a range of security processes and technologies to protect and keep your banking details secure. Our security controls have been rigorously tested by independent IT auditors. Our customers’ security is our biggest priority.

We will never:

ask for your password

send you an email or SMS asking for personal information

How can I protect myself?

The tips below can help to protect your personal and financial information from fraud and scams.

Emails

Do not open suspicious or unsolicited emails – delete them straight away.

Do not click on any links in a suspicious email, or open any attached files.

Don’t rush in. Resist the urge to “act now” despite the tempting offer. Once you turn over your money, it’s unlikely you’ll see it (or the product or service you’ve paid for) again.

Use up to date and comprehensive antivirus software.

SMS

Fraudulent SMS messages often feature similar characteristics to phishing emails. Popular SMS scams often reference “tracking a parcel” or “collecting your prize”.

Do not click on any links in a suspicious SMS.

We’ll never ask you to provide your personal information, credit card or bank account details or other payment information via SMS.

Remember, criminals can set the “Sender Name” of SMS messages to make it appear as though they’re being sent by someone other than themselves.

Fraudulent SMS messages will often ask you to click a link which directs you to a web page that isn’t part of Alex.Bank. If the link looks unfamiliar, it’s likely a scam.

Personal details

Never enter personal, credit card or bank account details on a website if you’re not certain it is genuine. Always check the website address as scammers create URLs that look remarkably similar.

Never send your personal, credit card or bank account details through an email.

Keep your passwords and PINs safe and don’t share them with anyone.

Check your credit card and/or bank statements regularly for suspicious transactions.

If you accidentally provide account or banking details to someone suspicious, you should contact your bank or financial institution immediately.

Phone calls

If you are in doubt about the authenticity of a call, don’t commit to anything. Instead, hang up and call the company directly. Never use contact details provided by the caller – find the number through their website or the White Pages.

If a bank or any other organisation phones you, don’t provide your personal details or any account or credit card numbers until you can verify the authenticity of the caller by using the tips above.

Where can I get help with cyber security?

Stay Smart Online & The Australian Cybercrime Online Reporting Network (ACORN) are now part of the Australian Cyber Security Centre (ACSC), the Australian Government’s online safety and security website.

Visit the ACSC website for resources to protect yourself online, such as:

SCAMwatch – Australian Competition and Consumer Commission website offering information about how to recognise, avoid and report scams.

Office of the Children’s eSafety Commissioner – Australian Government website with resources and advice to assist children who experience cyberbullying.

MoneySmart - Australian Government website providing financial resources and tools.

For further information on scams and how to protect yourself, visit the SCAMwatch website.

How do I check my data privacy and marketing permissions?

As part of applying for an Alex Bank product, we may from time to time send you news and updates regarding new products and promotions. If you don’t want to receive these, you can unsubscribe at any time by clicking on the ‘unsubscribe’ link at the bottom of emails.

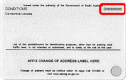

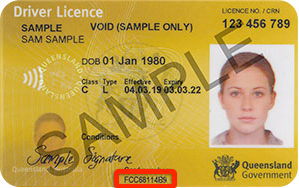

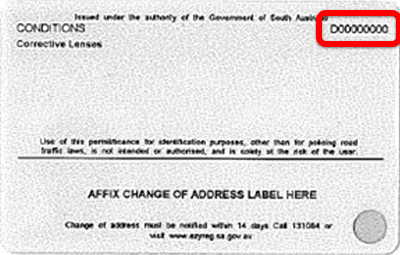

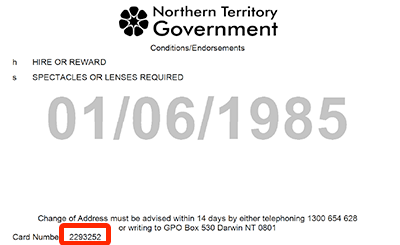

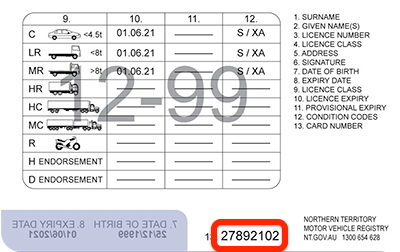

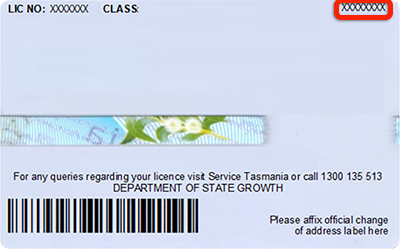

What is my Drivers Licence Card Number?

Your drivers licence card number is a unique identifier found on newer versions of Australian drivers’ licences. It is different to your drivers licence number. Both numbers can be found on your card.

Providing both your licence and card number when validating your identification ensures that the document presented is the most recently issued card. This reduces the risk of identity theft using lost or stolen drivers licences.

Your drivers licence card number varies slightly depending on the state the licence was issued:

New South Wales (NSW) 10 digits (numbers only)

Australian Capital Territory (ACT) 10 digits (numbers only)

Victoria (VIC) 8 characters (numbers and letters)

Queensland (QLD) 10 characters (numbers and letters)

Before Jun 2019

Since Jun 2019

Western Australia (WA) 8-10 characters (numbers and letters)

South Australia (SA) 9 characters (numbers and letters)

Northern Territory (NT) 6-8 digits (numbers only)

Example

Since Dec 2022

Tasmania (TAS) 9 characters (numbers and letters)

Complaints, Disputes, Hardship

How do I contact Alex Bank if I have a complaint?

You can contact our Brisbane based customer service team during regular business hours on 13 ALEX or email us at hello@alex.bank.

You can find out more information regarding complaints in our Complaints Policy.

Is there someone independent I can complain to?

Yes, you can lodge a complaint with the Australian Financial Complaints Authority.

What can I do if I'm experiencing hardship?

We know it’s not easy asking for help, but please don’t hesitate to contact us and let us know your circumstances so we can assist in any way we reasonably can. You can phone, chat or email us here

What can I do if I'm experiencing financial abuse?

Financial abuse is a form of domestic and family violence where one person manipulates another to control their finances without consent. This is a terrible experience and we know it’s not easy asking for help. Please don’t hesitate to contact us and let us know your circumstances so we can assist in any way we reasonably can. You can phone us on 13 ALEX or email us at hello@alex.bank

How long before I get a response to an enquiry, complaint or feedback?

We aim to get back to you within one business day.

About our banking licence

What is an ADI?

An Authorised Deposit-taking Institution (or ‘ADI’) is a financial institution in Australia that is supervised by the Australian Prudential Authority (APRA). Under the Banking Act 1959, ADI’s are authorised to accept deposits from the public and can offer bank accounts. All banks are covered under the Government’s Financial Claims Scheme (FCS), which protects money held in bank accounts up to a total value of $250,000 per person. Alex Bank is currently operating under an Authorised Deposit-taking Institution licence.

Who is APRA?

APRA is the Australian Prudential Regulation Authority, which is a regulator of the Australian banking and finance sector.